What Are the Executor's Responsibilities When Selling an Inherited Home?

Everything starts with authority. Before you can list, sign, negotiate, or sell, you need to know who actually has the legal right to make decisions and sign documents. That might be the executor named in the will, an administrator appointed by the court, a trustee, a surviving spouse, co-owners, or beneficiaries under specific circumstances.

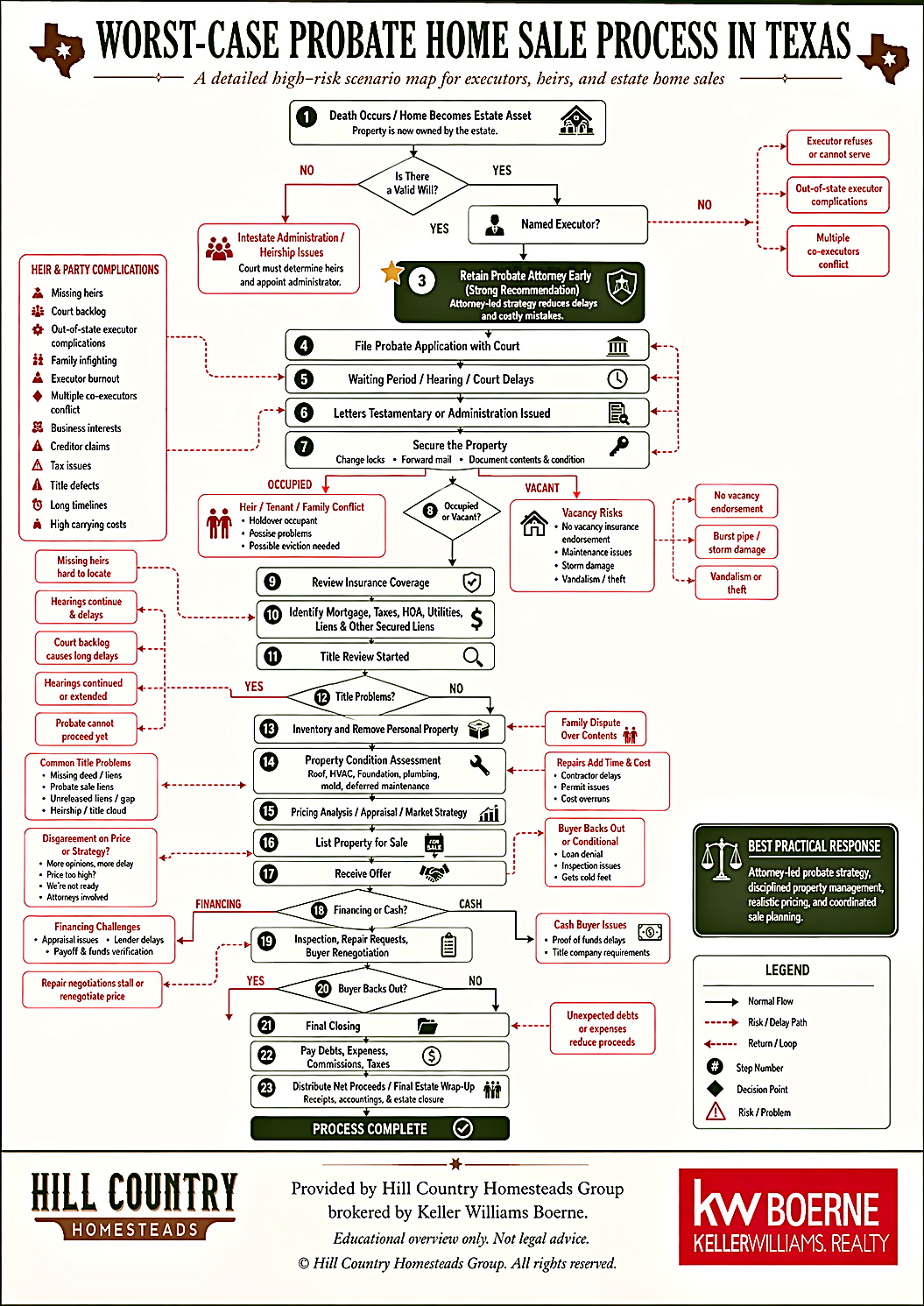

In Texas, approximately 67% of Americans die without an up-to-date will (Caring.com, 2024), meaning the court must appoint an administrator rather than relying on a named executor. When there is a will, about 70% of Texas estates proceed through independent administration, giving the executor broad authority under Texas Estates Code Chapter 401.

Don't assume the most vocal family member has authority. Authority comes from the court, not from family consensus. Verify it through proper legal channels.

"An independent executor has all the rights, powers, and duties conferred by the will or by law, and may act independently of and without the approval of any court."

Build Your Professional Core Team Early

The earlier you assemble the right professionals, the smoother the process moves. Your core team typically includes:

- Estate attorney — your legal guide through probate

- Real estate agent experienced with estate sales — someone who understands probate timelines and court coordination

- Title company — to surface liens, title defects, and ownership questions

- CPA — for tax implications of the sale and estate

- Insurance agent — to confirm coverage during the estate period

- Cleanout and estate-sale companies — for personal property

- Appraiser and contractors — for condition assessment

Build Your Working File and Timeline

Create a master file with the will, court filings, letters testamentary or administration, trust documents, deed, title policy, mortgage, taxes, HOA, insurance, utilities, surveys, repair invoices, and leases. Build a master timeline with legal milestones, property-security tasks, cleanout deadlines, listing-prep steps, court/title dependencies, and carrying costs by month.